While we do not know at this point how long this correction will last or what the ultimate decline will be, we do not believe that this is the start of a bear market in which the decline would be much deeper and last longer. In our view, a combination of improving economic data, evidence of the Fed getting a handle on inflation, and some diplomatic resolution in Eastern Europe will go a long way to getting the stock market back on solid footing and reestablishing the long-term bullish trend. While still early, Q4 earnings have generally been positive, with companies able to manage input costs through pricing and what appears to be a resilient consumer. At the end of the day, corporate profits drive stock market performance, and what we’ve seen thus far is indicative of a broader recovery.

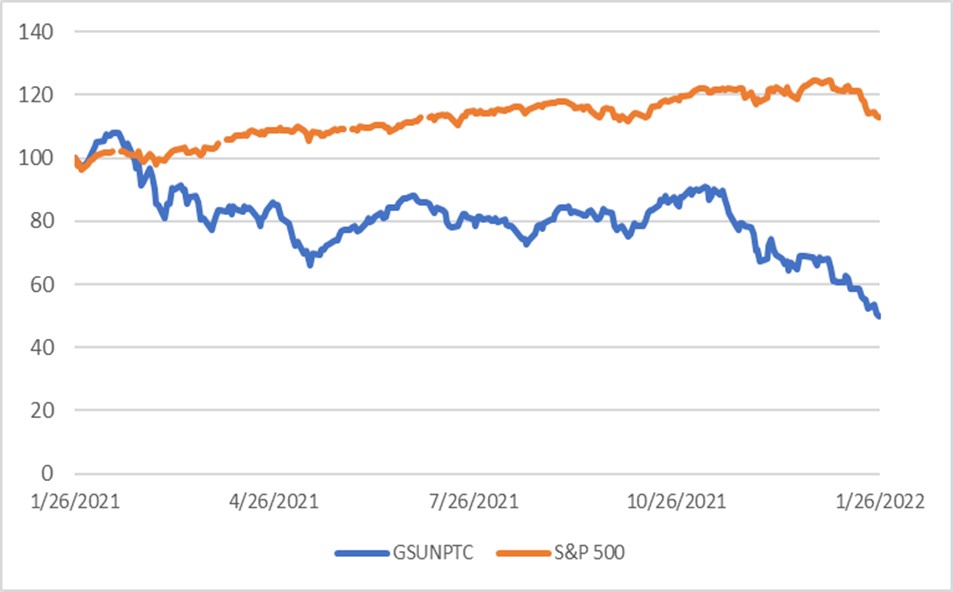

One other important point is that much of the negative headlines during this correction have focused on stocks with extremely high valuations that became “frothy” during the pandemic and Tech stocks with little or no earnings. To highlight this point, we present the one-year performance of the Goldman Sachs Non-Profitable Tech index versus the S&P 500.